CLINUVEL Newsletter

Dear shareholders, friends

On behalf of the CLINUVEL Board, I wish you all a good new year in the hope that it confers you with good health and prosperity, in that particular sequence. We thank and owe much to Stan McLiesh who retired on November 30 2019 after 17 years of service, we welcome Willem Blijdorp as new Chairman and also Professor Rosenfeld who is a welcome addition to the Board.

PROSPECTIVE CLINUVEL NEWS

In this first Communiqué of the new year we review the objectives following the US Food and Drug Administration (FDA) decision in October to approve the first ever treatment for patients with erythropoietic protoporphyria (EPP). As with previous years, material news flow in 2020 will depend on the activities of the Company and, given the frequency of developments in our business, we intend to maintain bi-monthly Communiqués. In addition, we will publish a number of Scientific Communiqués throughout the year. On evaluation, the high frequency of updates – 7 News Communiqués, 3 Scientific Communiqués, more than 75 social media releases and over 60 market announcements in 2019 – has been well received.

At the start of the year and with the “EPP season” nearing in the Northern hemisphere, our teams find themselves in the midst of preparing for all mandatory European activities, while the US discussions with payors and intermediaries are progressing to facilitate access to SCENESSE® (afamelanotide 16mg).1 Simultaneously, the FDA is reviewing the obligatory post-marketing protocol to ensure CLINUVEL will remain in compliance with its requirement to monitor American EPP patients for the duration of a minimum of eight years (up to 2027). As stated during the investor call on 9 October 2019, US distribution will be staged and depending on logistics, training & accreditation, final post-marketing authorization protocol signed off by the FDA before we will see patients on treatment.

At the start of our nineteenth year since the inception of CLINUVEL, the team has returned back from the Christmas break highly motivated to meet two key primary objectives; one to accelerate our innovative R&D programs; and two, to make SCENESSE® available in America.

While the past successes of our team are memorable, I regard our achievements merely as the foundation to advance CLINUVEL as if we had started a brand-new business on 1 January 2020. With a freshness and a positive attitude our teams need to keep an eye on the next set of challenges without bias from its past successes. We wish to see growth across all business areas.

The prospects of the Company are there for us to fulfil and our near-term aspirations were expressed in full during the 2019 AGM. Looking back at past performance, the focus on and deployment of SCENESSE® in EPP led to the current enterprise value. Our work towards specific objectives should see value increase at the back of:

- a. clinical progress in vitiligo;

- b. complementary OTC product(s);

- c. a new indication;

- d. investigation of DNA repair;

- e. expansion of R&D;

- f. US market access;

- g. Australian TGA submission accepted, initiation of the review; and

- h. European market expansion.

The rest of our prospective achievement then lies in the identification and mitigation of business risks as well as continued executional prowess.

US REGULATORY REQUIREMENTS & DISTRIBUTION

The new decade has started with CLINUVEL’s first meeting with the FDA; the formal Post-authorization Feedback Meeting. The FDA’s specialised division, primarily responsible for the evaluation of SCENESSE®, provided positive feedback on the scientific review. While the contents of the interaction between Company and the FDA remain part of confidential exchanges pledged under agreement, I took away from this meeting the confirmation by the agency of ‘the unusual nature of this scientific dossier and product’, without exact qualification of what constituted the distinguished features.

Nonetheless, we had assessed early on from the interactions with the FDA in its review (mirroring the interactions with the European Medicines Agency (EMA) during evaluation of the technical dossier), that SCENESSE® had posed complexities in its scientific assessment due to its innovative nature as a:

- (i) novel concept of systemic photoprotection;

- (ii) first in class;

- (iii) novel mode of action (pharmacology);

- (iv) novel formulation; and

- (v) new administration route.

In this respect CLINUVEL’s entire regulatory strategy to 2019 – and therefore dossier – was written towards the expectation that this technical dossier would pose a higher level of complexity to the FDA. On 8 January 2020, our previous assessment was confirmed by the US regulatory agency.

Since CLINUVEL expects to engage in frequent exchanges with the

same division of the FDA in the coming years, consistency in regulatory approach and public expression remains of ‘the essence’ and has perhaps become the hallmark of our undertakings; I truly hold that most of the Company’s successes are embedded in its consistency of communication with decision and policy makers.

The heightened regulatory attention to SCENESSE® as a new molecular entity is seen against the backdrop of a changing regulatory environment and recent critical press towards those who focus on orphan drugs. Not unsurprisingly, the EMA had waded through all publications released by and on the Company, both formal and informal write-ups, to assess whether CLINUVEL had remained in compliance with the European disclosure and advertising codes protected by the EMA. On a few occasions we had been asked or encouraged to modify the language on CLINUVEL’s website and remove what was perceived to be inappropriate definition of the lead treatment. Naturally, our communications and media team will remain vigilant to keep CLINUVEL in check, but it remains arbitrary how much one is able to discuss on an innovative treatment without crossing the perceived boundary. The same rigour to monitoring excess promotion of the first systemic photoprotective therapy is now applied by the FDA, albeit the open communications in making pharmaceutical products visible appears more acceptable in the US.

The targeted penetration rate (total percentage of a treatment reaching diseased patients) of a novel treatment is a question often received by our teams. In reference to the US studies by the IQVIA Institute, one finds that, for example, treatment of a disease with a prevalence of approximately 5,000 patients is shown as having an average 13.5% of clinical uptake, suggesting that identification and diagnosis of these very rare diseases remains uncertain.

Above: the impact of EPP is widely misunderstood

To counteract the known historic penetration rates of novel therapies, we had started the identification and monitoring of potential patients more than a decade ago. By using various channels, we are confident that the uptake of the SCENESSE® treatment by known EPP patients will be higher than the research suggested, based on current treatment and retention rates in the European Union, along with feedback received on US demand thus far. However, the total number of patients treated over the years will largely depend on a number of factors such as reimbursement, Medicare-Medicaid and payors’ preparedness to provide treatment for these patients and drug access.

The most limiting factor in treatment of US EPP patients would undoubtedly be the travel distance and vicinity to expert treatment centres. CLINUVEL’s approach is to “take the therapy to patients” by assigning centres to provide patients access within a reasonable radius. In retrospect of the planning needed during the US clinical trial program from 2010 to 2013, we facilitated transport at long distances for US EPP patients to reach study centres. We evaluated that the SCENESSE® therapy under real-world-commercial conditions would be easier to facilitate than during the US clinical trials, when the Company had to organise long distance travel by aeroplane and taxis, and accommodation for overnight stay close to clinical research sites. Our current activities are aimed at enabling access for those affected to be treated as outpatients and to return home the same day, limiting the impact of treatment on their lives. It would be remiss not to focus on the logistics of product distribution in the US, whilst more than ever, I wish our teams to keep these details close to their chest as part of the internal knowhow built with CLINUVEL. Market exclusivity granted by the US FDA and CLINUVEL’s position has come at a great cost and is of much value.

The same integrated systems as for the controlled distribution in the European Union are being erected in the US. It needs to be stressed that follow-up of patients’ post-authorisation is not only imposed by global regulators, but also a genuine mechanism to protect the well-being of our patients, to enable 24/7 medical access to the Company.

We will maintain our emphasis on the patients’ safety monitoring which assists us in all future programs of SCENESSE® and melanocortins. CLINUVEL’s global Qualified Person for Pharmacovigilance is overseeing and bearing the responsibility for the safety of the medicinal product in the European Economic Area and the US. Together with a tightly managed Global EPP Disease Registry (GEDR), the Company will be in an optimum position in the US. A most important outcome of the successful FDA review is the fact that all medical data can be harmonised in the GEDR to enable pooling of information and annual analyses on SCENESSE® to be submitted to EMA and the FDA. The EU and US protocols allow future pooling of data.

I would like to see our sector to evolve in a different direction, and why should CLINUVEL not lead in this regard?

Part of the business case CLINUVEL seems to be writing fits our view that a pharma company entering a new decennium should “treat its customers” significantly differently to the standard our peers have historically set. Therefore, CLINUVEL seeks to differentiate in its approach and life-long management of its primary and secondary customers – interpret here as patients and physicians. Some questions one ponders are along the following lines:

- how different would a patient and general public perceive the aftercare provided by a drug manufacturer if this company actually had shown a closer interest in the well-being of the recipient even after treatment had been provided and ceased?

- how different would it be to view the academic physicians and experts as part of a tripartite collaboration in development of novel products by offering them the opportunity to actively assist in the clinical programs?

In many other industries, customer management and after-care are key to a business’ long-term success. In pharmaceuticals, we traditionally provide a prescriptive therapy and leave the aftercare to the primary care physician. At CLINUVEL, we view the “customer relationships” quite differently and build robust systems to manage these relationships, reflecting a Company-wide approach to follow up and keeping close to our patients and prescribers. In doing so, CLINUVEL refrains from inducing, incentivising or paying physicians, since they all should remain independent at all times.

I believe that medical care by a modern-day pharmaceutical company should be longitudinal and systematic beyond the treatment effect of

a drug. This approach already heralded much positive feedback in Europe, and I would like to see us continue in a similar mode in the US.

When looking worldwide at the annual treatment cost per patient per annum, one can derive the Life-Time Value of an EPP patient. Assuming an average number of treatments per annum, it is easy to understand why CLINUVEL pays attention to maintaining an ‘arms-length’ relationship to its patients. The economic argument of knowing each individual patient’s profile (without actually receiving details of name, identification and address) is strong. Mathematically, modelling the value of long term follow up of both patients and physicians provides revealing sensitivities.

US PRICING OF SCENESSE®

Nevertheless, from popular press one can gauge that proposals are being tabled by the US Congress for pharmaceutical companies to disclose the list price of its products in advertisements. Ahead of the US presidential election in 2020, I expect there will be significant change to our sector in an attempt to attract a new electorate unified by dissatisfaction with the US health system and drug pricing.

In CLINUVEL’s 2019 AGM (AGM presentation slide deck), we discussed the changing political environment and CLINUVEL’s approach to the pricing and reimbursement of our drug. The reactions to CLINUVEL’s approach have been most positive thus far.

Many of the US insurance groups these past years had no notion of EPP and their awareness of it remained low in spite of numerous campaigns launched since 2014. We believe that the recognition to treat EPP patients has grown since 2016 and US payors are now starting to acknowledge the need to offer treatment to patients who have been ‘left in the dark since birth’.

CLINUVEL’s US pricing policy seems to set us apart from our peers and seems well timed in the current climate as the US Democratic and Republican movement brews over drug pricing reform. A number of US investment banks have picked up on CLINUVEL’s approach to uniform pricing and have posed questions related to why others have not followed this model. There is no faint attempt to read the motivations of others, and we can only elucidate how a global policy, fixing cross-border drug pricing, makes sense while the manufacturer continues to shoulder the economic burden of currency fluctuations, import levies, specialised shipping costs, pharmacovigilance and quality management systems.

A number of these relevant parameters are being discussed by US insurers and form part of negotiations.

The health economic value for the pharmaceutical product is based on a number of factors, including:

- comparable treatments to alleviate life-time burden of disease;

- number of available and treatable patients per continent;

- impact on national health budgets;

- proportionality and fairness to society; and

- the impact the treatment has on patients’ lives.

The dimension of the treatment effect is significant and needs to be supported by independent physicians as part of a value dossier.

An additional argument is that, in a globalised world of e-commerce, differential pricing becomes less logical as hospitals procure the cheapest available treatment worldwide through the parallel import of drugs. Physician groups have been formed internationally and exchange pricing conditions, while insurance groups are seen to exchange purchasing conditions and information. One can now add to that the emergence of Amazon which has stated its intention to play a global role in drug distribution. We believe major changes are pending.

In the dynamic interplay as sketched above, we shall elaborate in the future on the economic conditions and distribution of SCENESSE® as it becomes widely available for EPP patients in the US.

PUBLIC AND INVESTOR RELATIONS

The 2019 calendar year marked a further step-up in the extent of CLINUVEL’s communication with shareholders and stakeholders in general. The frequency and range of issues covered increased and was extended into other languages, reflecting the diversity of our shareholder base.

For example, in May 2019 we issued a communiqué in German (largely based on the April communiqué), for the benefit of our German speaking shareholders. We received positive feedback on this initiative which resulted in the formation of a German speaking distribution list. We will translate this communiqué to German and make it available on our website.

The feedback received on the value of this communiqué series in general has been encouraging and we will maintain this series for your understanding of our Company and its progress.

The period from the FDA’s milestone approval on 8 October 2019 through to the AGM on 20 November was a particularly intensive period for investor relations. Key CLINUVEL personnel across a range of geographies were involved in many meetings with existing and potential shareholders and other stakeholders to communicate the developments in the business. CLINUVEL received extensive media coverage of the FDA’s approval and we were pleased to have one of the highest shareholder turnouts ever at the AGM. Shareholders may care to review the following media CommSec interviews, an Australian outlet: CommSec1 in October and CommSec2 in December. We appreciate the reactions of shareholders to the results achieved and the range of questions on the Company asked at the AGM was of interest.

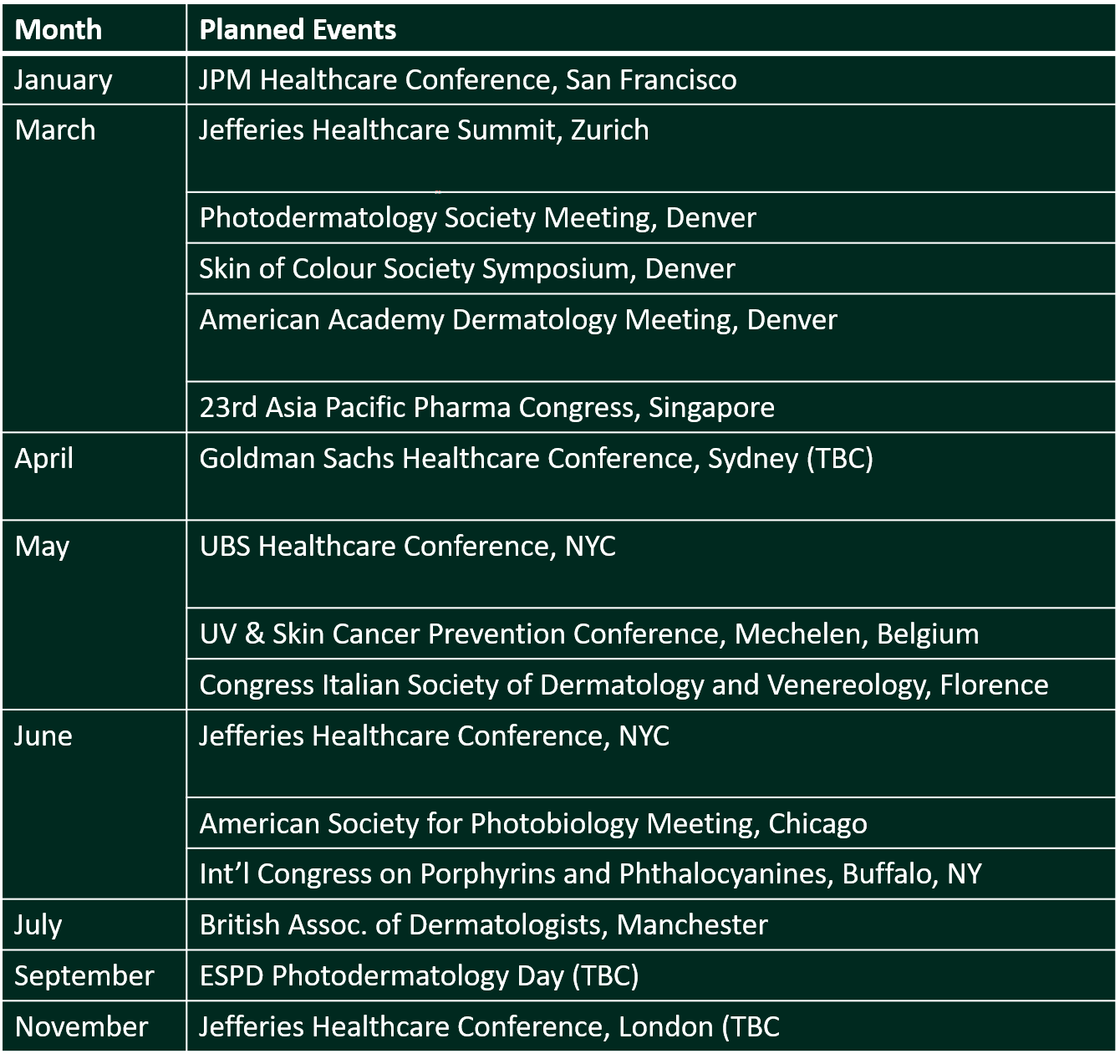

In 2019 we started sharing CLINUVEL’s participation in key events around the world. Following a tradition started last year, we illustrate below the healthcare conferences which CLINUVEL intends to present at or attend during 2020.

As this communiqué is issued, CLINUVEL is attending the JPM Healthcare Conference in San Francisco. This is the world’s most significant healthcare gathering and we will tell the CLINUVEL story there as we meet industry and financial sector representatives and institutional investors.

We share the extensive presence of CLINUVEL for 2020. At most of the conferences listed in the table, CLINUVEL will present its story and plans, while several managers will also exhibit CLINUVEL’s Exhibition Space to targeted audiences at the same or other industry-specific events. The list is not exhaustive and will be refined as we receive confirmation on some of those listed and other events.

SUMMARY

We conclude this first News Communiqué for 2020 with well-founded optimism that our Company is positively poised for further growth. Focus at most critical times and commitment from our entire team who blaze a trail are the ingredients for us to realise potential. I look forward to providing you further updates as our journey continues.

Philippe Wolgen

1SCENESSE® (afamelanotide 16mg) is approved in the European Union as an orphan medicinal product for the prevention of phototoxicity in adult patients with EPP. SCENESSE® is approved in the USA to increase pain free light exposure in adult EPP patients with a history of phototoxicity. Information on the product can be found on CLINUVEL’s website at www.clinuvel.com.