Appendix 4D Half Year Report

Results For Announcement To The Market

|

($A’000) |

||||

|---|---|---|---|---|

|

Revenues from continuing activities |

Increased |

58% |

to |

15,743 |

|

Profit from continuing activities after tax attributed to members |

Increased |

962% |

to |

6,487 |

|

Net Profit for the period attributed to members |

Increased |

962% |

to |

6,487 |

Dividends (Distribution)

| Amount per security | Franked amount per security | |

|---|---|---|

| Final dividend (prior year)* | 2.5 ¢ | Unfranked |

| Interim dividend | *Nil ¢ | *Nil ¢ |

| *CLINUVEL PHARMACEUTICALS LIMITED paid the dividend on 18 September 2020 | ||

| Previous corresponding period (31 December 2019) | 2.5 ¢ | Unfranked |

| Record date for determining entitlements to the dividend | N/A | N/A |

Brief explanation of any of the figures reported above and short details of any bonus or cash issue or other item(s) of importance not previously released to the market:

* Not applicable

Commentary on Results

For commentary on the results of CLINUVEL PHARMACEUTICALS LIMITED please refer to the Result of the Consolidated Entity and the Review of Operations in the attached Directors’ Report. The information in the Half Year Report should be read in conjunction with the details and explanations provided herewith, along with the most recent Annual Report.

NTA Backing

|

Current Period |

Previous Corresponding Period |

|

|---|---|---|

|

Net tangible asset backing per ordinary security |

$1.48 |

$1.35 |

Other Information

Control gained or lost over entities having material effect – n/a

Dividends (in the case of a trust, distributions) – n/a

Details of aggregate share of profits (losses) of associates and joint venture entities – n/a

CLINUVEL PHARMACEUTICALS LIMITED A.B.N. 88 089 644 119

AND CONTROLLED ENTITIES HALF YEAR FINANCIAL REPORT ENDED

31 DECEMBER 2020

Directors’ Report

Your Directors present their report on the Company and its controlled entities for the half year ended 31 December 2020.

Directors

The names of Directors in office at any time during or since the end of the half year are:

• Dr. K. E. Agersborg;

• Mr. W. Blijdorp;

• Prof. J. V. Rosenfeld;

• Mrs. B. M. Shanahan;

• Mrs. S. E. Smith;

• Dr. P. J. Wolgen.

Directors have been in office since the start of the financial year to the date of this report unless otherwise stated.

EXECUTIVE SUMMARY & KEY HIGHLIGHTS FOR THE HALF YEAR ENDING 31 DECEMBER 2020

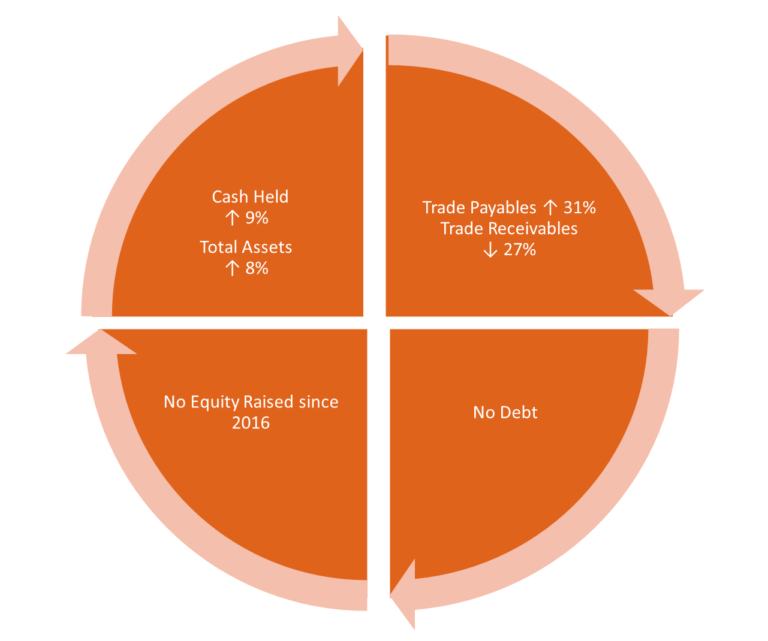

We find ourselves in the midst of the worst recession since the Great Depression of 1929 impacting many businesses and households. CLINUVEL continuously aims to attain independence and build shock absorbers to ensure sustainability and operational confidence to the medical community, patients, shareholders, and our suppliers. Whilst there have been record capital raises in life sciences in Australia, CLINUVEL has not been forced to depend on external sources to finance to its operations. In general, companies raised capital at a discount to the prevailing market prices which had dilutionary consequences to shareholders.

The key to return to normalcy lies with the tireless dedication of governments and healthcare workers not only treating those infected, but also ensuring mass vaccination of the population. In parallel, societies will need to find an answer to human losses and economic ravage; substantial debt has been incurred by governments and enterprises which have tried to sustain economic activity through the crisis. While consensus forecast a 26% increase in earnings per share in developed countries, economic recovery for small businesses and families is expected to consume many years.

CLINUVEL’s financial management is systematic, disciplined and focussed to navigate the Company long-term through economic adversities. Our relentless strategy is focussed on building a sustainable platform of drug candidates for patient populations with high unmet medical need. Recently, the Group announced its development of accompanying suite of over-the-counter (OTC) products to complement its pharmaceutical offerings, expanding in dermocosmetics.

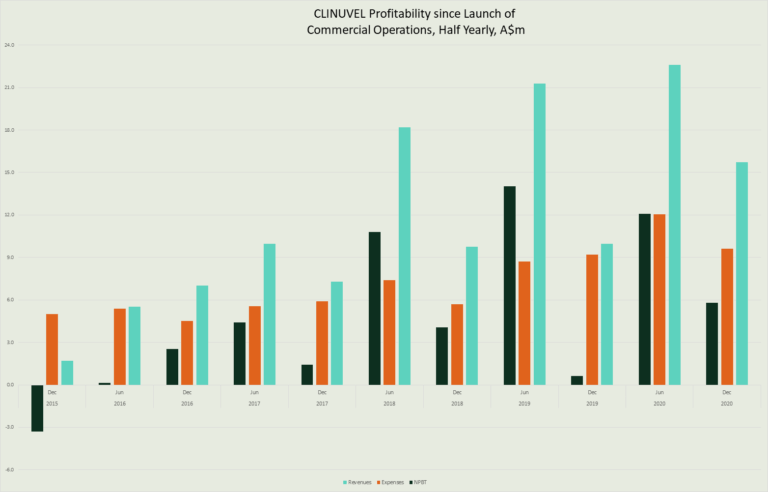

Overturning the legacy of failed corporate progress from 1987 to 2005, the Company has implemented its turnaround strategy the past 15 years to develop SCENESSE® (afamelanotide 16mg) in a comprehensive clinical trial program establishing its safety and efficacy. This strategy led to the approval of the lead pharmaceutical product by European Medicines Agency (EMA), US Food and Drug Administration (FDA) and Australian Therapeutic Goods Administration (TGA) for the treatment of adult patients diagnosed with erythropoietic protoporphyria (EPP).

Our approach led to first revenues recorded from European sales in June 2016 and in the USA in April 2020, underpinning five years of positive cashflow and profitability. CLINUVEL has built cash reserves to finance commercial operations and expand the Group.

In navigating various recessions and delays in obtaining regulatory and reimbursement clearance, we have been able to adapt, manage and grow the business in the recent year, despite the disruption in supply chains experienced.

Reflecting the outlined strategy, the Group achieved positive results in the half year to 31 December 2020:

• Improved revenues to $15.743 million, up 58% compared to the prior corresponding period (pcp);

• A 9% increase in cash held to $72.918 million, providing a robust foundation to finance further growth and expansion;

• A net profit of $6.487 million, up 962%, the tenth consecutive half year profit result and a record result for a December half year;

• An expense result of $9.621 million, up 5% on the equivalent period last year, reflecting the Company’s increased investment in the expansion of its R&D and commercial activities to meet its strategic objectives, as recently outlined in the October 2020 update;

• A balance sheet comprising no debt and net equity of $78.084 million; and

• Positive earnings per share of $0.13 an increase of 956% on the same period last year, reflecting the change in profit result period-on-period.

| Consolidated Entity |

6 Months Ended 31-Dec-20 |

6 Months Ended 31 Dec 2019 Restated |

Change |

|---|---|---|---|

| $ | $ | % | |

| Revenues | 15,743,215 | 9,971,065 | 58% |

| Net Profit before income tax | 5,810,821 | 610,660 | 852% |

| Profit after income tax expense | 6,487,320 | 610,660 | 962% |

| Basic earnings per share | 13.3 | 1.3 | 956% |

| Net tangible assets backing per share | 1.481 | 1.351 | 10% |

RESULT OF THE CONSOLIDATED ENTITY (‘GROUP’) AND BALANCE SHEET

The Group result for the half year ended 31 December 2020 was a $6.487 million net profit after income tax expense. This is the Group’s tenth consecutive half year profit result and a record result for a first half year in which revenue is typically lower than the second half of the financial year due to the changes in seasonal demand (cooler months) for SCENESSE® in the northern hemisphere. The net profit result for the half year ended 31 December 2020, was 962% higher than the pcp result.

Despite the economic downturn, the Group pursued its commercial operations in the European Economic Area and made progress in its commercial operations in the USA. Overall, revenues rose 58% to $15.743 million in the half year ended 31 December 2020, whilst expenses rose by 5% to $9.621 million in supporting the growth of commercial operations and the research and development, as announced in the October 2020 Strategic Update. The profit margin before tax was up 37% in the reporting period.

Key highlights of the financial activities of the consolidated entity for the six months to 31 December 2020 follows:

FINANCIAL HIGHLIGHTS

Balance Sheet

One of the key objectives of the Company is to ensure its Balance Sheet is sufficiently robust to allow investment in its pipeline products with a financial buffer to respond to unexpected systemic adverse economic events. The Company has continued to preserve cash and cash equivalents and, in doing so, is able to withstand anticipated increases in short-term liabilities to support the business expansion.

Key Balance Sheet highlights of the reporting period:

The balance sheet was strengthened by positive cash flows from the Company’s commercial distribution program in the EU and the USA, increasing cash reserves by 9%, from $66.747 million at 30 June 2020 to $72.918 million at 31 December 2020.

A strong balance sheet was maintained, with net assets increasing by 8.4% from $72.067 million at 30 June 2020 to $78.0854 million. There was no debt or equity capital raised in the current or previous reporting period. Net tangible assets increased to $1.48 per share. The current ratio as at 31 December 2020 is 935% (30 June 2020: 910%).

In September 2020, the Board of Directors declared an unfranked dividend of $0.025 per share, resulting in a net distribution to shareholders and a reduction in the Group’s cash and cash equivalents of $1.235 million (September 2019: $1.224 million).

Revenues

The Group achieved Total Revenues of $15.743 million for H1-FY2021, a 58% increase on the result to the pcp of $9.971 million.

A comparison of the H1-FY2021 ‘reported’ and ‘constant currency’ results against the H1-FY2020 ‘reported’ results for Commercial Sales and Special Access Scheme (SAS) Reimbursements is shown below:

| A$ million | H1-FY2021 Reported | H1-FY2021 Constant* | H1-FY2020 Reported | % change |

|---|---|---|---|---|

| Commercial Sales | 13.633 | 13.858 | 7.394 | 87.4 |

| SAS Reimbursements | 2.11 | 2.099 | 2.577 | -18.5 |

* FY2021 revenues converted to A$ monthly at the average conversion rate of the same month used for FY2020.

Commercial Sales

On a constant currency basis revenue from the distribution of SCENESSE® increased 87% in the six months to 31 December 2020 compared to the pcp. This result was driven by a combination of:

• US revenues booked for the first time in a December half year. Commercial sales in the USA commenced in the latter part of FY2020, starting with supply to one EPP Specialty Center. As of the 31 December reporting date, 34 Specialty Centers had been trained and accredited to administer SCENESSE® and more than sixty private insurers, both national and local, have agreed to reimburse SCENESSE®;

• European EPP Expert Centres located in regions severely affected by COVID-19 in the first half of calendar year 2020 not placing orders until the current reporting period;

• European EPP Expert Centres ordering earlier than in prior years and increasing their inventories to prescribe to patients during 2021;

• Further increases in new patients enrolled under the post-authorisation safety study and treated by EPP Expert Centres before and during lockdown; offset by,

• EPP patients in some countries who would normally seek treatment in the cooler months opting to avoid treatment and not travelling to their EPP Expert Centre for treatment, or hospital protocols requiring some physicians to avoid treating EPP patients to prioritise their response to the coronavirus pandemic.

Despite the most challenging economic conditions from the coronavirus pandemic in Europe impacting patient access during the second half of FY2020 when demand for SCENESSE® generally increases, CLINUVEL continued to supply European EPP Expert Centres prescribing SCENESSE®.

In the US, CLINUVEL has been assisting EPP patients and Specialty Centers to confirm reimbursement with insurers under Prior Authorization (PA) and generally working to ensure access to treatment and subsequent reimbursement of the cost of treatment. The acceptance of SCENESSE® by insurers and patients, with repeat treatments occurring, bodes well for future supply.

The price of SCENESSE® in Europe remained constant in FY2020 and through to 31 December 2020, in line with CLINUVEL’s policy to charge a uniform net price across all European countries.

Reimbursements – Special Access Schemes

The distribution of SCENESSE® under Special Access Schemes continued to provide a preventative treatment for adult EPP patients, primarily in Switzerland. SCENESSE® was also exceptionally supplied outside Switzerland under a special access arrangement. CLINUVEL received cost compensation for SCENESSE® (provided in non-Euro currency to take account of exchange rate movements against the Euro in the prior calendar year).

On a constant currency basis, reimbursements from Special Access Schemes decreased 18.5% in the six months to 31 December 2020 compared to the pcp. This reflects the receipt of orders earlier in the 2020 calendar year when compared to 2019 and the impact of some patients not travelling to the EPP Expert Centre to seek treatment. On a calendar year basis, however, the number of units under Special Access Schemes increased by 6.7%, a positive outcome given the treatment difficulties caused by the coronavirus pandemic.

Other Income

The Group’s exposure to holding funds in non-Australian dollar currency, combined with revaluing end date trade debtors and creditors from their original currency into Australian dollar presentation currency, contributed to the Group reporting an unrealised foreign currency movement loss of $0.551 million for H1-FY2021 (H1-FY2020 loss: $0.509 million).

The Group recorded other income of $0.084 million in government grants received in Australia and Singapore to assist companies to respond to the economic impact of the COVID-19 pandemic. The Group also benefited from realising exchange rate gains on transactions in non-Australian currency throughout the period of $0.026 million (pcp: $0.029 million).

Interest Income

Interest received from funds held in bank accounts and term deposits for H1-FY2021 generated $0.217 million in interest income compared to $0.309 million for H1-FY2020, a 30% decrease.

The positive financial performance of the Group saw an increase to its cash reserves, and this resulted in an average 25% more cash held in higher-yielding Australian dollar fixed rate term deposits compared to the pcp. The increase to average cash balances earning a fixed term deposit rate was balanced out by a lower average interest rate of 47 basis points earned on these funds when compared to the prior period. The decline in average term deposit rates reflects the impact of Australian government monetary policy on term deposit rates on offer throughout the period, the outcome of two rate cuts to the cash rate since 31 December 2019.

Expenditures

The expense result of $9.621 million in the half year ended 31 December 2020, was up 5% on the pcp, reflecting the Company’s increased investment in its research and development program and expanded activities to meet its strategic objectives, as outlined in the October 2020 Strategic Update. Commentary on specific expense categories follows.

Clinical Development

Clinical development fees increased 75% from $0.094 million in H1-FY2020 to $0.165 million in H1-FY2021.

The Group has prioritised its commercialisation activities in Europe and in the US, while making advances in its regulatory and clinical activities. Expenses towards clinical development represent approximately 1% of total expenses in each year since 2014,the year of European regulatory approval. The Group recently announced an update where it revealed a two-pronged strategy to scientifically translate its technologies, developing prescription medicines for life-threatening disorders as well as making its technologies available for non-prescriptive healthcare solutions.

The increase in the clinical development expense result reflects the pursuit of this strategy, with investments in:

• the set-up of a pilot Phase II study (CUV801) to evaluate the safety and efficacy of afamelanotide in arterial ischaemic stroke;

• the set-up of a pilot Phase II study (CUV150) in xeroderma pigmentosum (XP); and

• product development and testing services on Healthcare Solutions products by the VALLAURIX subsidiary.

Drug formulation R&D, manufacture & distribution

Expenses toward further research, development, manufacture and optimisation of drug and product formulations and the freighting and distribution to the end user decreased 11%, from $1.110 million in H1-FY2019 to $0.986 million in H1-FY2021.

The Group continues to invest in its manufacturing supply chain to prepare for future sales growth and to meet short-term and long-term inventory requirements. Development and manufacture of active ingredients continued to support re-supply and further improvement to manufacturing processes across our platform technologies continued. Further investment in our distribution systems was made to ensure implants were able to be provided to customers throughout a challenging period from the coronavirus pandemic along with UK’s eventual departure from the EU. Drug formulation R&D also includes the development work and usage of derivative peptide material within the VALLAURIX Singapore operations.

This expense result for H1-FY2021 was driven by:

• positive regulatory initiatives in managing the implant supply chain resulting in cost savings;

• increased costs in implementing the distribution systems and freighting goods to US Specialty Centers; and

• further costs in ensuring the right distribution systems are in place to facilitate implant supply into and in Europe after the post-transition Brexit Date of 1 January 2021.

Regulatory (Pre- & Post-Marketing) & Non-clinical

Regulatory and non-clinical fees decreased 2% from $0.876 million for H1-FY2020 to $0.860 million in H1-FY2021.

Fees related to regulatory affairs for post-marketing activities are directly related to the Group meeting its ongoing regulatory compliance activities to distribute SCENESSE® in Europe and the USA. These activities include pharmacovigilance, safety reporting worldwide, PASS registry data capture and dossier updates. Pre-marketing regulatory expenses are the costs incurred by the Group to prepare, submit, and manage the submissions to regulatory agencies to approve the use of SCENESSE® in EPP. As part of the Group’s strategic intent to expand the use of melanocortins in other severe disorders, non-clinical activities are performed to support the scientific rationale of afamelanotide and related molecules as a proof of concept. Regulatory and non-clinical fees also include the support required for pricing dossier submissions.

This expense result for H1-FY2021 was driven by:

• reduced spending on external pharmacovigilance services as a component of these functions are returned in-house;

• new fees connected to investigational work into UV-induced DNA skin damage, aiming to show the benefit of afamelanotide and further molecules in non-clinical modelling; and

• increased fees associated with pricing dossier applications, filings, and price negotiations with payors to reimburse SCENESSE® across Europe.

Clinical, Regulatory & Commercial overheads

Clinical, Regulatory & Commercial (‘C,R&C’) overhead costs increased 26% to $2.037 million in the six months ended 31 December 2020 (31 December 2019: $1.617 million).

As part of CLINUVEL’s longer term objectives, increasing the C,R&C personnel headcount is considered an essential investment to:

• drive new product development programs in our internal innovation centre, VALLAURIX PTE LTD;

• establish and grow the commercial distribution program in the USA;

• further sustain the ongoing commercial activities in Europe, and

• investigate the further use of SCENESSE® in indications other than EPP to expand its market potential.

The half year to 31 December 2020 follows the trend seen in FY2020 of increasing C,R&C staff count in these key business areas to drive organic growth. As the company continues to expand, C,R&C overheads will follow.

This expense result for FY2020 was driven by:

• growth in headcount in Australia, the UK, Singapore, and the USA; and

• volume increases to manufacturing royalty fees from first-time US commercial revenues.

Business marketing & listing

Business marketing and listing fees decreased 18% from $0.882 million for the six months ended 31 December 2019 to $0.727 million for the current period.

This expense result was driven by a severe downturn in activities following the outbreak of the coronavirus, which saw a decrease of expenses due to the inability to physically engage in face-to-face meetings with expert audiences at industry exhibitions and financial conferences.

Despite the decline in these activities, the Group proceeded in its focus of building a broader online awareness of the CLINUVEL brand to support the communicating of the Group’s updated strategic focus to expand the use of prescription medicines based on melanocortins and to develop new technology via new OTC products. The Company continued to invest in more in-house marketing resources to support the building of CLINUVEL’s brand exposure and to prepare for launch the OTC products.

Patents and trademarks

Patents and trademark charges saw a 12% increase, from $0.150 million in the same period last year to $0.168 million in the current period. The Group continues to maintain and validate its existing portfolio of patents and trademarks across key jurisdictions, providing essential market protection and a competitive advantage over other actual and/or potential competitors.

This expense result was driven by:

• investments in trademarks of new product names including PRÉNUMBRA®, CLINUVEL’s new non-solid (liquid) presentation of drug candidates, as well as undisclosed product names for new non-prescriptive products in development as part of the Healthcare Solutions Division;

• further fortification of the intellectual property position on the new product development and complementary formulations within the VALLAURIX business; and

• further maintaining, strengthening, and validating the position of the existing patent portfolio, including patent term extension requests.

General operations

Expenditures from general operations increased 22% from $3.781 million in H1-FY2020 to $4.596 million in H1-FY2021.

General operations are reflective of the support function necessary to ensure the execution of the Company’s demanding near-term and long-term expansion strategy. General operations comprise costs including the remuneration of senior management along with IT, corporate support, legal, Board fees and various non-cash items.

This expense result for H1-FY2021 was driven by:

• increases to the non-cash depreciation and right-of-use charges connected to the relocation and renovation of its advanced centralised Research, Development & Innovation Centre in Singapore, operating through the VALLAURIX PTE LTD subsidiary; and

• non-cash expensing of share-based payments, the accounting charge directly related to the approval by shareholders of performance rights to the Managing Director at the 2019 Annual General Meeting and for which expensing only commenced in November 2019.

Other

Other expenses decreased 91% to $0.063 million in H1-FY2021 (H1- FY2020: $0.667 million). The decrease was attributable to the cessation of nearly all staff travel in the current reporting period.

Deferred Tax Asset

The Group has brought to account a deferred tax asset (DTA) relating to previously unrecognised prior period tax losses. resulting in a credit to income tax benefit of $0.676 million (pcp: $nil). The amount of the DTA brought to account reflects:

• the benefit to be received from utilising unused tax losses against the temporary differences that result in a deferred tax liability for the business; and

• the expected utilisation of unused tax losses against probable near term taxable profits.

Earnings per share

The Group was able to increase its earnings per share. Basic earnings per share for the period ended 31 December 2020 was $0.133 on a weighted average number of 48,639,785 issued ordinary shares, compared to the 31 December 2019 result of: $0.013 basic earnings per share on 48,339,167 weighted average issued ordinary shares.

Review of Operations

Company Overview

CLINUVEL PHARMACEUTICALS LTD is a global and diversified biopharmaceutical company focused on developing and commercialising treatments for patients with genetic, metabolic, and life-threatening disorders, as well as healthcare solutions for the general population. As pioneers in photomedicine and understanding the interaction of light and human biology, CLINUVEL’s research and development has led to innovative treatments for patient populations with a clinical need for systemic photoprotection, DNA repair and acute or life-threatening conditions. These patient groups range in size from 5,000 to 45 million worldwide.

CLINUVEL’s lead compound, SCENESSE® (afamelanotide 16mg), was approved by the European Commission in 2014, the US FDA in 2019 and the Australian TGA in 2020 for the prevention of phototoxicity (anaphylactoid reactions and burns) in adult patients with EPP.

CLINUVEL’s headquarters is in Melbourne, Australia with operations in Europe, Singapore, and the USA.

Objectives

The Group vision is to innovate medical and healthcare solutions for unmet needs. We actively work to translate scientific concepts and breakthroughs into commercial products. We are determined in our desire to excel scientific research and development, building on our global expertise to deliver lifelong care and novel products for patients and consumers.

The long-term financial objective of the Group is to maximise company value through the distribution of treatments to patients in need. The key to long-term profitability of the Group is:

• continuing the successful research and development of a portfolio of assets centred around its key drug candidate SCENESSE®;

• successful commercialisation, manufacture, and distribution; and

• maintenance of financial discipline and stability.

A key facilitator of these objectives is the ability to attract funding to support CLINUVEL’s activities, should the need arise.

Performance Indicators

Management and the Board monitor the overall performance of the Group in relation to its strategic plan and annual operating and financial budgets.

The Board, with Management, have determined a range of key performance indicators (KPIs) that are used to monitor ongoing performance. Key managers monitor performance against these KPIs and provide regular reports to the Board for review, feedback, and guidance, as necessary. This enables the Board to actively monitor and guide the Group’s performance.

Dynamics of the Business

The key dynamics of the business are:

• The commercial operations of the Group, which are currently conducted in the European Economic Area and the USA.

– The European subsidiaries are concentrated on working with trained and accredited European EPP Expert Centres to provide SCENESSE® to patients with EPP, working within the commitments agreed with the EMA as a condition for continuous marketing authorisation;

– In October 2019, the FDA granted marketing approval to distribute SCENESSE® to increase pain-free light exposure in adult patients with a history of phototoxic reactions from EPP in the USA. This significant regulatory approval milestone has enabled the Group to increase its revenue base. Commercial operations were launched in April 2020.

• There is a degree of seasonality to CLINUVEL’s cash receipts which are markedly higher in the northern hemisphere during spring and summer when ambient light is more intense and demand for treatment from EPP patients is higher than in autumn and winter;

• CLINUVEL has agreed with EU payors a uniform net price per unit of SCENESSE®, reflecting the Group’s values of fairness and equitable treatment of all prescribers, and is applying this policy in the USA;

• SCENESSE® is manufactured in the USA by a sole contract manufacturer and is distributed by the Group directly to accredited EPP Expert Centres and Specialty Centers;

• The Group has an ongoing clinical interest to further develop SCENESSE®, encompassing:

– a DNA Repair Program, initially focussed on xeroderma pigmentosum (XP) and healthy volunteers;

– arterial ischaemic stroke (AIS);

– vitiligo, a skin depigmentation disorder, in North America; and

– variegate porphyria (VP), a disease indication belonging to the same family of disorders as EPP (porphyrias).

• The Melbourne headquarters of the Group covers the regulatory affairs, scientific programme, finance, and investor relations functions.

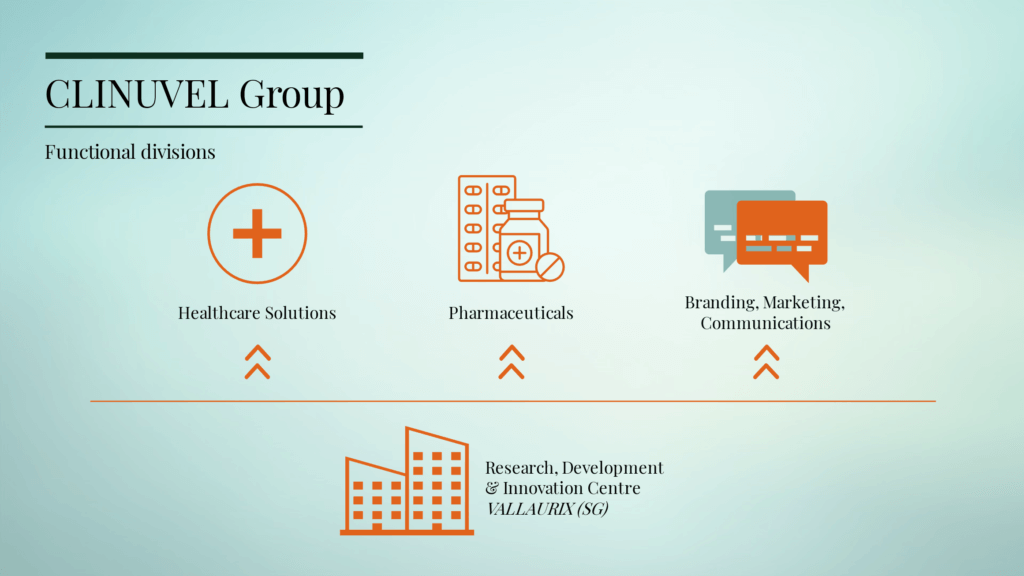

• The Group is organised into three divisions:

– Pharmaceuticals, the core division of the business focussed on melanocortin based pharmaceutical treatments for a wide range of indications;

– Healthcare Solutions, focussed on non-pharmaceutical products for a wider audience with a need for photoprotection and repair of DNA damage; and

– Communications, Branding and Marketing, to engage broader audiences for CLINUVEL’s products.

Underlying this structure is the Research, Development & Innovation Centre in Singapore, operated by the fully owned subsidiary, VALLAURIX PTE LTD which conducts the Group’s product development program.

Operational Overview

European Distribution of SCENESSE®

The supply of SCENESSE® to EPP Expert Centres across key European countries, including under a Special Access Scheme in Switzerland, continued in the half-year ended 31 December 2020. The majority of Expert Centres in Europe have continued to prescribe SCENESSE® to meet ongoing patient demand for treatment. A small number of Centres had either deferred orders or reduced order sizes in the initial months of the coronavirus pandemic, impacting the June quarter of 2020. In subsequent months, access to patients resumed with the easing of restrictions across Europe and has largely normalised. Despite the ongoing uncertainty surrounding the pandemic, patient demand for SCENESSE® has remained high and Expert Centres are working to facilitate ongoing treatment.

Progress of SCENESSE® for EPP in the USA

From FDA approval on 8 October 2019, the Group immediately focussed on the implementation of the US expansion plan. This involved:

• reaching agreement with the FDA on the pharmacovigilance protocol to apply for the next eight years to monitor the safety of SCENESSE® in patients with EPP;

• activation of a network of Specialty Centers to administer SCENESSE®;

• restructuring internal resources to implement quality management and pharmacovigilance systems;

• recruitment of a local team to support operational activities; and

• negotiation of agreements on reimbursement of the cost of treatment with US insurers.

Ahead of schedule, by 31 December 2020, the CLINUVEL team had trained and accredited 34 Speciality Centers to administer SCENESSE® which exceeded internal targets of 30 planned Specialty Centers by the end of 2021. Over 60 private insurers had agreed to reimburse the cost of treatment, mainly under PA arrangements, but also accepted SCENESSE® as a special drug or as part of their formulary listing. To enable the smooth process of reimbursement, the CLINUVEL team has worked with insurers and Specialty Centers on obtaining PA on a patient-by-patient basis and with key authorities to agree on the treatment code to be used in relation to SCENESSE®. An important event during the reporting period was the approval of code J7352 for SCENESSE® as “Afamelanotide implant, per 1 mg dose” by the Healthcare Common Procedure System. The code allows greater access to treatment as insurers now have a standardised way of recognising the treatment. A Savings Program for US EPP patients has also commenced to assist with out-of-pocket expenses.

SCENESSE® for EPP in other markets

Underpinned by the regulatory approvals in Europe and the USA, along with the information generated from its post-marketing commitments in Europe, the Group continues to work towards gaining regulatory approval for SCENESSE® for EPP patients in other markets worldwide.

In this regard, CLINUVEL applied to the Australian TGA in December 2019 to register SCENESSE® on the Australian Therapeutic Goods Register as a treatment for patients with EPP. The TGA approved SCENESSE® in October 2020 as the first therapy for adult patients with EPP in Australia. Australia is the third geographic region of the world in which regulatory approval of SCENESSE® has been obtained. Work continues to obtain its listing on the Pharmaceutical Benefits Scheme for reimbursement.

Efforts continue to progress regulatory approval in other markets. Post the reporting period, the Company announced in February 2021 that SCENESSE® was granted market access in Israel, extending the regulatory approvals of SCENESSE® to a fourth geographic region.

Product Pipeline

The Group has active product research and development pipeline activities with a focus on novel treatments for patients with severe genetic and vascular disorders who lack therapeutic alternatives. The pipeline includes research and development into:

• a paediatric formulation of SCENESSE®;

• DNA Repair, with an initial focus on the reparative properties of melanocortins on XP;

• SCENESSE® for AIS;

• SCENESSE® for adult vitiligo patients;

• next generation products based on melanocortin analogues CUV9900, parvysmelanotide and phimelanotide with the intention of developing these analogues for medicinal purposes to be administered topically; and

• a range of OTC products for general photoprotective and reparative application.

The Group continues to pursue a clinical program to evaluate the effectiveness of SCENESSE® to activate and repopulate melanocytes within vitiliginous lesions (depigmented skin areas) and achieve repigmentation in combination with narrowband UVB (NB-UVB) phototherapy in patients with vitiligo. Data from the clinical and pre-clinical studies evaluating efficacy and/or safety of SCENESSE® in combination with NB-UVB should result in the Group moving towards later stage clinical trials. A Type C Guidance meeting was held with the FDA in April 2020 to discuss the design of a multicentre Phase IIb clinical study in the US and the data package necessary to support a supplemental New Drug Application (sNDA) filing for SCENESSE® in vitiligo. Work has continued with clinical experts on the protocol of a multicentre Phase IIb clinical study of SCENESSE® in combination with NB-UVB, to treat vitiligo and we expect agreement to be reached in 2021.

The Company’s key research and development activities in the half year to December 2020 included:

• progress in the development of a second formulation of afamelanotide, PRÉNUMBRA®. Announced in July 2020, this liquid controlled-release formulation is to be evaluated in clinical trials for acute disorders and vascular anomalies;

• the completion of the Group’s new Research, Development & Innovation Centre in Singapore which opened at the end of August 2020;

• the announcement of an innovative DNA Repair Program in September 2020 which aims to confirm that intervention with SCENESSE® enhances the elimination of photoproducts and regeneration of DNA.

– This concept is being assessed first in the rare genetic disorder XP. The first XP-C patient was treated in September and during the monitoring period, the treatment was tolerated well. This confirmed the product’s safety, enabling us to move to the next step of Phase II study (CUV150) involving a group of six XP-C patients, subject to ethics committee and other approvals.

– As part of the DNA Repair Program, ethics committee approvals were granted to commence a Phase II study (CUV151) in ten healthy individuals who will be irradiated with UV to assess the skin damaged provoked by UV and the repair mechanisms assisted by afamelanotide. Subject to COVID-19 restrictions, readouts on these studies are expected in 2021.

• the research and development program was expanded in October 2020 to evaluate the effects of afamelanotide in patients suffering from AIS. Pending COVID-19 restrictions, a pilot Phase II study (CUV801) will commence to administer afamelanotide to up to six AIS patients to evaluate its safety and effectiveness. Readout on this study is anticipated in 2021.

• ongoing research and development into topical over-the-counter products with the first polychromatic protective product to be released later in 2021.

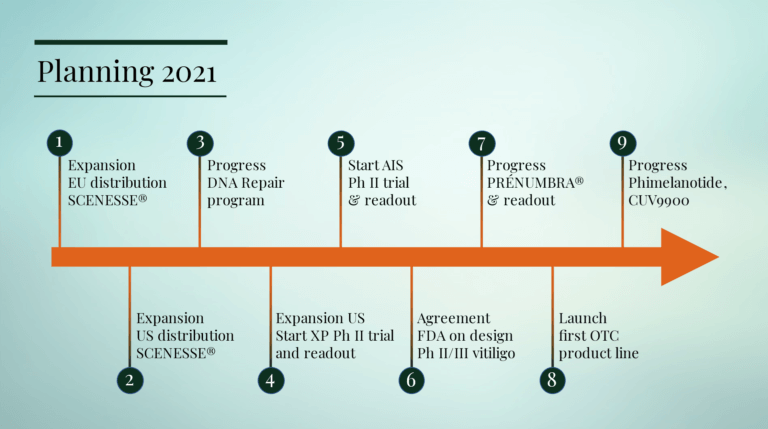

The October 2020 strategic update outlined the Group’s new divisional structure and expanded research and development program to support the diversification and growth of the Group in pharmaceutical products for unmet medical needs and non-pharmaceutical products for wider healthcare use. The nine key objectives of the CLINUVEL team in 2021 are outlined below:

Included in this document is the Half Year Report Appendix 4D, together with the Financial Report, this Directors’ Report and Declaration and Audit Independent Review Report relating to the half year ended 31 December 2020.

This Half Year Report forms part of this announcement to the Australian Securities Exchange Limited and should be read in conjunction with CLINUVEL’s Annual Report for the year ended 30 June 2020.

AUDITOR INDEPENDENCE DECLARATION

The independence declaration of our auditor as per section 307C of the Corporations Act is attached and forms part of the Directors’ Report.

Signed in accordance with a resolution of the Board of Directors made pursuant to section 306(3) of the Corporations Act 2001.

DR PHILIPPE WOLGEN

MANAGING DIRECTOR

Dated this 23rd day of February, 2021

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE HALF YEAR ENDED 31 DECEMBER 2020

| 31 December 2020 | 31 December 2019 Restated | |

|---|---|---|

| $ | $ | |

|

Revenues |

||

| Commercial sales of goods | 13,633,153 | 7,394,291 |

| Sales reimbursements | 2,110,062 | 2,576,774 |

|

Total revenues |

15,743,215 | 9,971,065 |

| Interest income | 216,707 | 309,016 |

|

Total interest income |

216,707 | 309,016 |

|

Other Income (loss) |

||

| Government grants | 83,597 | – |

| Realised net currency gain on transactions | 26,485 | 29,490 |

| Gain (loss) on disposal of property, plant and equipment | (86,958) | 107 |

| Unrealised loss on restating foreign currency creditors | (550,798) | (509,311) |

| and currencies held | ||

|

Total other income (loss) |

(527,674) | (479,714) |

|

Expenses |

||

| Clinical, Regulatory & Commercial overheads | 2,037,401 | 1,617,278 |

| Drug formulation R&D, manufacture & distribution | 986,184 | 1,110,469 |

| Regulatory (Pre & Post Marketing) & Non-clinical | 860,199 | 875,552 |

| Business marketing & listing | 726,741 | 882,198 |

| Licenses, patents and trademarks | 167,718 | 149,965 |

| Clinical development | 165,098 | 94,270 |

| General operations (incl. Board) | 4,596,360 | 3,781,452 |

| Finance costs | 19,223 | 11,137 |

| Others | 62,503 | 667,386 |

|

Total expenses |

9,621,427 | 9,189,707 |

|

Profit/(loss) before related income tax expenses |

5,810,821 |

610,660 |

| Income tax (expense)/benefit | 676,499 | – |

| Profit after income tax expense | 6,487,320 | 610,660 |

|

Net profit for the year |

6,487,320 |

610,660 |

|

Other comprehensive income |

||

| Items that may be re-classified subsequently to profit or loss | ||

| Exchange differences of foreign exchange translation of foreign operations | (440,340) | 552,137 |

| Income tax (expense)/benefit on items of other comprehensive income | – | – |

| Other comprehensive income/(loss) for the period, net of income tax | (440,340) | 552,137 |

|

Total comprehensive income for the period |

6,046,980 |

1,162,797 |

| Basic earnings per share – cents per share | 13.3 | 1.3 |

| Diluted earnings per share – cents per share | 12.7 | 1.2 |

This statement of profit or loss and other comprehensive income should be read in conjunction with the accompanying notes to the financial statements.

STATEMENT OF FINANCIAL POSITION

AS AT 31 DECEMBER 2020

| 31 December 2020 | 30 June 2020 Restated | |

|---|---|---|

| $ | $ | |

|

Current assets |

||

| Cash and cash equivalents | 72,918,097 | 66,746,521 |

| Trade and other receivables | 4,836,287 | 6,612,684 |

| Inventories | 1,316,154 | 1,287,914 |

| Other assets | 1,215,277 | 508,818 |

| Total current assets | 80,285,815 | 75,155,937 |

|

Non-current assets |

||

| Property, plant and equipment – net | 1,526,623 | 1,075,441 |

| Right-Of-Use assets – net | 1,395,575 | 1,313,937 |

| Intangible assets – net | 185,030 | 185,030 |

| Deferred tax assets – net | 4,487,999 | 3,811,500 |

| Total non-current assets | 7,595,227 | 6,385,908 |

|

Total assets |

87,881,042 |

81,541,845 |

| Current liabilities | ||

| Trade and other payables | 4,990,541 | 4,771,581 |

| Lease liabilities | 238,586 | 212,331 |

| Provisions | 3,358,352 | 3,278,176 |

| Total current liabilities | 8,587,479 | 8,262,088 |

| Non-current liabilities | ||

| Lease liabilities | 1,136,310 | 1,107,224 |

| Provisions | 72,424 | 105,727 |

| Total non-current liabilities | 1,208,734 | 1,212,951 |

|

Total liabilities |

9,796,213 |

9,475,039 |

| Net assets | 78,084,829 | 72,066,806 |

| Equity | ||

| Contributed equity | 151,849,375 | 151,849,375 |

| Reserves | 2,606,150 | 1,850,375 |

| Accumulated losses | (76,370,696) | (81,632,944) |

|

Total equity |

78,084,829 |

72,066,806 |

This statement of financial position should be read in conjunction with the accompanying notes to the financial statements.

STATEMENT OF CHANGES IN EQUITY FOR THE HALF YEAR ENDED 31 DECEMBER 2020

| Share Capital | Performance Rights Reserve | Foreign Currency Translation Reserve | Retained Earnings | Total Equity | |

|---|---|---|---|---|---|

| $ | $ | $ | $ | $ | |

|

Balance at 1 July 2019 |

151,314,175 | 654,324 | 698,092 | (95,486,738) |

57,179,853 |

| Issue of Share Capital under share-based payment | 535,213 | (535,213) | – | – | – |

| Employee share-based payment options | – | 437,461 | – | 26,704 |

464,165 |

| Dividends paid | – | – | – | (1,224,020) |

(1,224,020) |

|

Transactions with owners |

151,849,388 |

556,572 |

698,092 |

(96,684,054) |

56,419,998 |

| Profit for the half year | 1,059,248 | 1,059,248 | |||

| Prior Year Restatement | (448,588) | (448,588) | |||

| Restated profit for the half year | 610,660 | 610,660 | |||

| Other comprehensive income: | |||||

| Exchange differences of foreign exchange translation of foreign operations | – | – | 547,687 | – | 547,687 |

| Prior Year Restatement | – | – | 4,450 | – | 4,450 |

| Restated Exchange differences of foreign exchange translation of foreign operations | – | – |

552,137 |

– |

552,137 |

| Total other comprehensive income | – | – |

552,137 |

– |

552,137 |

| Balance at 31 December 2019 Restated | 151,849,388 | 556,572 | 1,250,229 | (96,073,394) | 57,582,795 |

| Balance at 1 July 2020 | 151,849,375 | 1,751,223 | 105,235 | (80,037,286) | 73,668,547 |

| Prior Year Restatement | (6,083) | (1,595,658) | (1,601,741) | ||

| Balance at 1 July 2020 restated | 151,849,375 | 1,751,223 | 99,152 | (81,632,944) | 72,066,806 |

| Issue of Share Capital under share-based payment | – | – | – | – | – |

|

Employee share-based payment options |

– | 1,196,115 | – | 10,194 |

1,206,309 |

| Dividends paid | – | – | – | (1,235,266) |

(1,235,266) |

| Transactions with owners | 151,849,375 | 2,947,338 | 99,152 | (82,858,016) | 72,037,849 |

| Profit for the year | 6,487,320 | 6,487,320 | |||

|

Other comprehensive income: |

|||||

| Exchange differences of foreign exchange translation of foreign operations | – | – | (440,340) | – | (440,340) |

| Total other comprehensive income | – | – | (440,340) | – | (440,340) |

| Balance at 31 December 2020 | 151,849,375 | 2,947,338 | (341,188) | (76,370,696) | 78,084,829 |

This statement of changes in equity should be read in conjunction with the accompanying notes to the financial statements.

STATEMENT OF CASH FLOWS FOR THE HALF YEAR ENDED 31 DECEMBER 2020

| Share Capital | Performance Rights Reserve | Foreign Currency Translation Reserve | Retained Earnings | Total Equity | |

|---|---|---|---|---|---|

| $ | $ | $ | $ | $ | |

|

Balance at 1 July 2019 |

151,314,175 | 654,324 | 698,092 | (95,486,738) |

57,179,853 |

| Issue of Share Capital under share-based payment | 535,213 | (535,213) | – | – | – |

| Employee share-based payment options | – | 437,461 | – | 26,704 |

464,165 |

| Dividends paid | – | – | – | (1,224,020) |

(1,224,020) |

|

Transactions with owners |

151,849,388 |

556,572 |

698,092 |

(96,684,054) |

56,419,998 |

| Profit for the half year | 1,059,248 | 1,059,248 | |||

| Prior Year Restatement | (448,588) | (448,588) | |||

| Restated profit for the half year | 610,660 | 610,660 | |||

| Other comprehensive income: | |||||

| Exchange differences of foreign exchange translation of foreign operations | – | – | 547,687 | – | 547,687 |

| Prior Year Restatement | – | – | 4,450 | – | 4,450 |

| Restated Exchange differences of foreign exchange translation of foreign operations | – | – |

552,137 |

– |

552,137 |

| Total other comprehensive income | – | – |

552,137 |

– |

552,137 |

| Balance at 31 December 2019 Restated | 151,849,388 | 556,572 | 1,250,229 | (96,073,394) | 57,582,795 |

| Balance at 1 July 2020 | 151,849,375 | 1,751,223 | 105,235 | (80,037,286) | 73,668,547 |

| Prior Year Restatement | (6,083) | (1,595,658) | (1,601,741) | ||

| Balance at 1 July 2020 restated | 151,849,375 | 1,751,223 | 99,152 | (81,632,944) | 72,066,806 |

| Issue of Share Capital under share-based payment | – | – | – | – | – |

|

Employee share-based payment options |

– | 1,196,115 | – | 10,194 |

1,206,309 |

| Dividends paid | – | – | – | (1,235,266) |

(1,235,266) |

| Transactions with owners | 151,849,375 | 2,947,338 | 99,152 | (82,858,016) | 72,037,849 |

| Profit for the year | 6,487,320 | 6,487,320 | |||

|

Other comprehensive income: |

|||||

| Exchange differences of foreign exchange translation of foreign operations | – | – | (440,340) | – | (440,340) |

| Total other comprehensive income | – | – | (440,340) | – | (440,340) |

| Balance at 31 December 2020 | 151,849,375 | 2,947,338 | (341,188) | (76,370,696) | 78,084,829 |

This statement of changes in equity should be read in conjunction with the accompanying notes to the financial statements.

NOTES TO THE CONDENSED FINANCIAL STATEMENTS FOR THE HALF YEAR ENDED 31 DECEMBER 2020

STATEMENT OF ACCOUNTING POLICIES, GENERAL INFORMATION AND

BASIS OF PREPARATION OF THE HALF YEAR FINANCIAL REPORT

The half year financial report is a general-purpose financial report prepared in accordance with the Corporations Act 2001 and AASB 134 Interim Financial Reporting. The half year financial report does not include notes of the type normally included in an Annual Report and shall be read in conjunction with the most recent annual financial report.

NEW AUSTRALIAN ACCOUNTING STANDARDS ISSUED THIS YEAR

AASB 2020-4 Amendments to Australian Accounting Standards – Covid-19 – Related Rent Concessions

AASB 2020-4 amends AASB 16 to provide a practical expedient that permits lessees not to assess whether rent concessions that occur as a direct consequence of the covid-19 pandemic and meet specified conditions are lease modifications and, instead, to account for those rent concession as if they were not lease modifications. The adoption of the amendment standards had minimum or no impact to the Group’s financial statements.

CONTINGENT LIABILITIES AND ASSETS

There are no known significant contingent liabilities or contingent assets as at the date of this report.

DIVIDENDS PAID OR RECOMMENDED

A final unfranked dividend for 2020 of 2.5 cents per share was paid on 18 September 2020 and a final unfranked dividend for 2019 of 2.5 cents per share was paid on 19 September 2019.

RESTATEMENT OF COMPARATIVE AMOUNTS

The Group has restated its comparatives for the year ended 30 June 2020 and half year ended 31 December 2019 in these consolidated statements after re-assessing the accounting treatment of the Loyalty Payment employee benefit granted to the Managing Director upon the renewal of his employment contract in October 2019, the benefit disclosed in the Remuneration Report to the 2020 Annual Report. The re-assessment of the treatment of the benefit determined the amount to be recognised over its service period commencing at the time of renewal of employment agreement to its vesting date.

The impact of this treatment on the 31 December 2019 profit and loss is an overstatement of profit of $0.449 million.

There is no impact on the cash flow position of the Group reported as at 31 December 2019 as the adjustment represents a non-cash entry.

The accounting treatment has been corrected by restating each of the affected financial statement line items for the prior period as follows:

| Balance Sheet (extract) | 30 June 2020 | Increase/(Decrease) | 30 June 2020 (Restated) |

|---|---|---|---|

| Provisions-current | 1,676,435 | 1,601,741 | 3,278,176 |

| Liabilities – current | 6,660,347 | 1,601,741 | 8,262,088 |

| Liabilities – total | 7,873,298 | 1,601,741 | 9,475,039 |

| Net Assets | 73,668,547 | (1,601,741) | 72,066,806 |

| Reserves | 1,856,458 | (6,083) | 1,850,375 |

| Accumulated losses | (80,037,286) | 1,595,658 | (81,632,944) |

| Total Equity | 73,668,547 | (1,601,741) | 72,066,806 |

| Statement of profit or loss and other comprehensive income (extract) | 31 December 2019 | Increase/(Decrease) | 31 December 2019 |

| (Restated) | |||

| General operations (incl Board) | 3,332,864 | 448,588 | 3,781,452 |

| Profit/(loss) before related income tax expenses | 1,059,248 | (448,588) | 610,660 |

| Net Profit for the year | 1,059,248 | (448,588) | 610,660 |

| Other comprehensive income/(loss) for the period, net of income tax | |||

| 547,687 | 4,450 | 552,137 | |

| Total comprehensive income for the period | 1,606,935 | (444,138) | 1,162,797 |

Earnings Per Share

Basic Earnings Per Share

Basic earnings per share is determined by dividing net profit after income tax attributable to members of the Company, excluding any costs of servicing equity other than ordinary shares, by the weighted average number of ordinary shares outstanding during the financial year, adjusted for bonus elements in ordinary shares issued during the year.

Diluted Earnings Per Share

Diluted earnings per share adjusts the figures used in the determination of basic earnings per share to take into account the after income tax effect of interest and other financing costs associated with dilutive potential ordinary shares and the weighted average number of shares assumed to have been issued for no consideration in relation to dilutive potential ordinary shares.

Basic earnings per share were $0.133 on a weighted average number of 48,639,785 issued ordinary shares. This compares with restated basic earnings per share of $0.013 as at 31 December 2019 on a weighted average number of 48,339,167 issued ordinary shares.

Events Subsequent To Balance Date

There has not been any matter that has affected, or could significantly affect, the operations of the Consolidated Entity subsequent to balance date.

Revenue

There has not been any matter that has affected, or could significantly affect, the operations of the Consolidated Entity subsequent to balance date.

| Six months to 31 December 2020 | Six months to 31 December 2019 | ||||||

|---|---|---|---|---|---|---|---|

| Commercial sales of goods | Sales reimbursements | Total | Commercial sales of goods | Sales reimbursements | Total | ||

| $’000 | $’000 | $’000 | $’000 | $’000 | $’000 | ||

| Europe & USA | 13,633 | 95 | 13,728 | 7,394 | 23 | 7,417 | |

| Switzerland, Others | – | 2,015 | 2,015 | – | 2,554 | 2,554 | |

| Total | 13,633 | 2,110 | 15,743 | 7,394 | 2,577 | 9,971 |

The Group’s revenue disaggregated by pattern of revenue recognition is as follows: the Group recognises all revenue based on a point in time.

SEGMENT REPORTING

A segment is a component of the Consolidated Entity that earns revenues or incurs expenses whose results are regularly reviewed by the chief operating decision makers and for which discrete financial information is prepared.

The Group has identified its operating segments based on the internal reports that are reviewed and used by the Chief Executive Officer (the Chief Operating Decision Maker) in assessing performance and in determining the allocation of resources. The Group operates in a single operating segment, being the biopharmaceutical sector, and the majority of its activities are concentrated on researching, developing and commercialising a sole asset, being its leading drug candidate. Accordingly, the Group’s consolidated total assets are the total reportable assets of the operating segment.

The Group has established entities in more than one geographical area. The non-current assets that are not held within Australia are immaterial to the Group. The revenues earned from external customers by geographical location is detailed above. The consolidated entity has one operating segment within the definition of AASB 8 Operating Segments.

Directors’ Declaration

In the opinion of the Directors:

1. The financial statements and notes, of the company and of the Consolidated Entity, are in accordance with the Corporations Act 2001, including:

(a) giving a true and fair view of the Consolidated Entity’s financial position as at 31 December 2020 and its performance for the half year ended on that date;

(b) with Accounting Standard AASB134 Interim Financial Reporting and the Corporations Regulations 2001; and

2. There are reasonable grounds to believe that the Company will be able to pay its debts as and when they become due and payable.

This declaration is made in accordance with a resolution of the Board of Directors pursuant to section 303(5) of the Corporations Act 2001.

DR PHILIPPE WOLGEN

Director

Dated this 23rd day of February, 2021